LUKOIL / OFAC — Executive Signal (GL 131B)

What changed

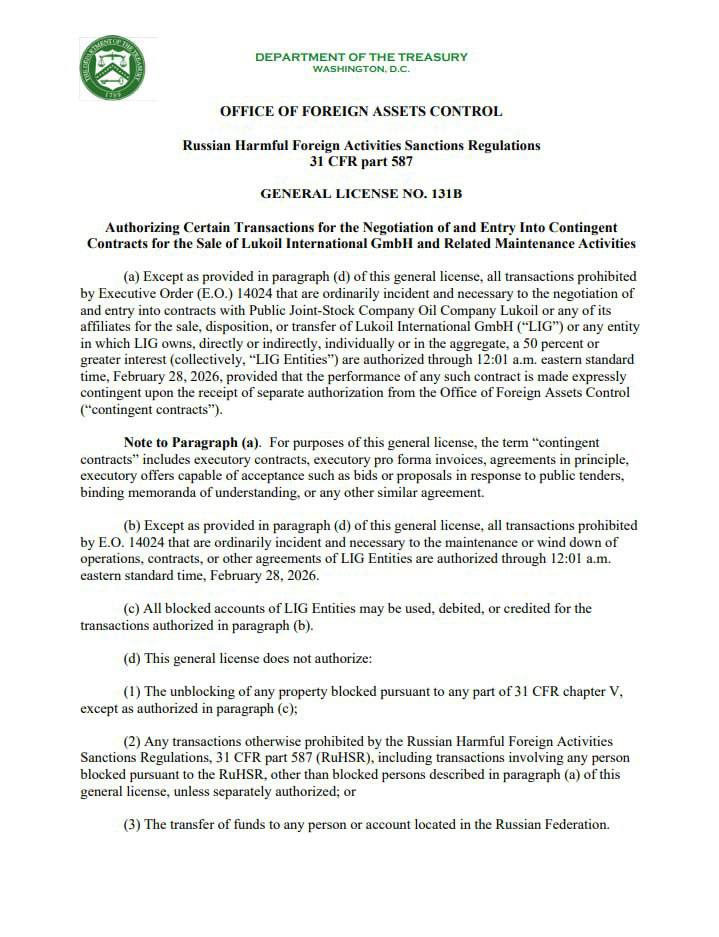

- OFAC issued/extended General License 131B under the Russian Harmful Foreign Activities Sanctions Regulations (31 CFR Part 587).

- Authorises U.S.-person transactions that are ordinarily incident and necessary to:

- Negotiate and enter into “contingent contracts” for the sale/disposition/transfer of Lukoil International GmbH (LIG) and covered LIG entities through 28 Feb 2026 (12:01 a.m. ET).

- Maintain or wind down operations/contracts/agreements of LIG entities through 28 Feb 2026 (12:01 a.m. ET).

- Key limitation: this is not blanket approval for a sale. Any contingent contract must be expressly contingent on separate OFAC authorisation before it can be performed.

What it is (and what it isn’t)

- Procedural time extension to keep a controlled pathway open for diligence, negotiation, and operational continuity.

- Not a deal announcement and not evidence a transaction has closed.

Hard constraints (compliance reality)

- No general unblocking of property beyond what the licence narrowly permits.

- No authorisation for other prohibited RuHSR transactions outside the licence scope.

- No transfer of funds to any person/account located in the Russian Federation (explicitly prohibited in the licence text).

Market impact

- Crude/products flows: Neutral near-term. Assets continue operating under restrictions; no “Russian barrels return” mechanism here.

- Narrative risk: reduces headline volatility by signalling sanctions pressure is being managed via ownership pathways, not by relaxing supply restrictions.

- European refining assets exposure (Romania/Bulgaria/Netherlands): operational continuity, strategic uncertainty persists; ownership transition risk remains the main variable.

Most likely path (base case)

- Asset-sale remains possible but not enabled automatically; execution still requires separate OFAC approval.

- Buyer talk (market chatter, unconfirmed): Chevron + Quantum Capital Group, potentially split-asset structure.

What to watch next

- Any specific licence or public filing indicating OFAC approval to perform a contingent contract (that’s the real “deal signal”).

- Changes in operating posture at LIG-linked EU assets: capex freezes, turnaround timing shifts, procurement tightening.

- Banking/payment routing constraints tightening/loosening (especially anything testing the “no funds to Russia” line).

Bottom line

Time-buying, not resolution. Neutral for prices today, but ownership and compliance execution risk stays elevateduntil a licensed sale is actually approved and consummated.